Table of Contents

The tax considerations of being self employed in Australia are unique. Legally minimising your tax burden and taking advantage of every available deduction requires careful and informed forward planning of tax minimisation strategies.

If undertaken without professional guidance, tax management can be riddled with missed opportunities for claiming tax benefits. Unanticipated and unnecessarily large tax bills, interest charges and fines can result.

In this article, taxation management strategies for the self employed are outlined. Registering a business as a sole trader, identifying and preparing for the types of taxes applicable to sole traders, the setting up of bookkeeping routines for tax minimisation and the creation of a business tax management plan are covered.

What is self employment anyway? How do I know if I am self employed?

A “Self employed” person in Australia can be a gig worker, an independent contractor servicing one or more companies/clients, or a business owner-operator (who may or may not employ others).

Like casual workers, the self employed do not receive holiday or sick pay from an employer. Unlike casuals, they do not have income tax withheld on their behalf from payments made to them.

It is possible to be both self employed and employed by another business at the same time; when engaging in gig economy or contracting work on top of regular employment, for example.

OK, I’m self employed what do I need to do to pay my tax?

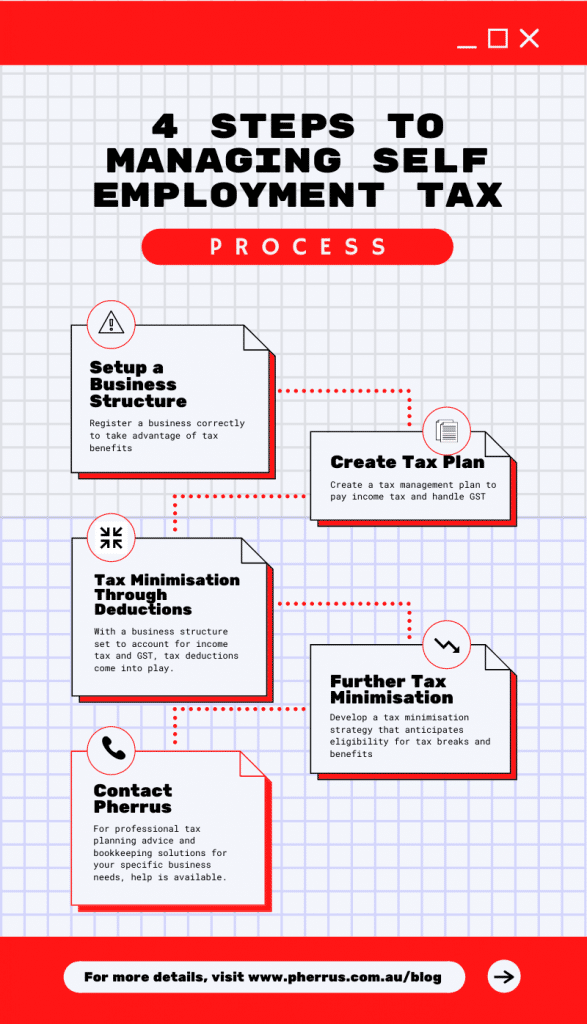

It requires planning to minimise tax burden on your business activities legally and effectively. There are four main action points to a taxation management and minimisation strategy for the self employed:

– Register a business and set up a business structure to take advantage of tax benefits

– Create a tax management plan to pay income tax and handle GST

– Establish bookkeeping for tax minimisation through deductions

– Develop a tax minimisation strategy that anticipates eligibility for tax breaks and benefits

Each of these steps is briefly outlined later in this article. Whilst this information serves as a handy overview for the independent entrepreneur to begin to take charge of their tax, the details may be overwhelming without the kind of preparation provided by a professional taxation consultant. Receiving an unexpected Australian Tax Office (ATO) notice following a self-prepared, first year self employed tax return can be panic-inducing.

For example, a mandatory Pay-As-You-Go (PAYG) instalment request, following a tax return, can leave the tax layman throwing their hands up in the air shouting: “What, self employed tax Australia-based?”

If that is a familiar feeling, contact the experts at Pherrus Financial Services to take control of your tax situation right away.

4 steps to managing self employment tax

Step 1: Register a business and set up a business structure to take advantage of tax benefits

Sole proprietorship is the simplest and least costly way to set up a taxation structure for declaring self employed income. Any self employed person is able to register a business with the ATO as a “sole trader” to gain access to tax advantages.

The sole trader business structure simply means a business is managed and operated by a single owner, who has unlimited liability and legal responsibility for all aspects of the business.

Registering as a sole trader is accomplished by applying for an Australian Business Number (ABN). This is an 11-digit identifier that can be displayed on your invoices, email signature, paperwork, business cards and website. An ABN can be obtained by filling out an application online at the Australian Government Business Registration Service portal.

Although ABN registration is not compulsory in all cases, it confers a number of instant benefits, such as avoiding a 47% GST withholding on payments made by other businesses to the sole trader.

With an ABN established, the sole trader is in a position to take advantage of tax deductions and tax breaks available to businesses. Self employed entitlements are key to tax minimisation and require the development of a year-round bookkeeping routine to secure.

Once an ABN has been registered, a sole trader’s name can be used to perform a free, publicly accessible online ABN search. Being listed for search self employed register tools, such as the ABN Lookup tool on the Business Register website, allows clients, customers and other businesses to identify the ABN holder as a self employed sole trader.

Step 2: create a tax management plan to pay income tax and handle GST

Income tax

As a self employed sole trader, all revenue earned through business activities is taxed as income.

When getting a new venture off the ground, taxation is often back-of-mind for the first-year self employed. Tax-free thresholds apply to income derived from self employment the same way they do for income gained through regular employment; that is, the self employed do not pay income tax on their first $18,200 of revenue.

A first year self employed tax free return can create a false expectation of tax reporting, obligation burdens and possible penalties once the business grows to attract revenue exceeding the tax free threshold.

For those who are self employed but working for an employer as well, declaring self employed income is done in tandem with declaring income from the regular job.

The combination of incomes from the first year of self employment activity and the regular job can push an earner into a new tax bracket and increase the income tax rate applicable to their business income, creating an unexpectedly large tax bill, especially if nothing has been set aside.

There is also the possibility of a new business taking off straight away. After reaching the tax-free threshold level of earnings, self employed sole traders need to track which income tax bracket rate is applicable to each new payment they receive so that the appropriate amount of income tax on that payment is reserved.

Adding to this amount set aside for income tax, an additional percentage for the Medicare levy needs to be reserved (an amount of up to 2% of income after the first $22,801 of earnings). Opening a savings account and depositing income tax and Medicare levy installments as payments are received helps to avoid a shock on an annual return.

After a tax return showing a change in income due to being in business for yourself, the ATO may issue a notice to begin paying income tax in quarterly installments – a Pay As You Go (PAYG) arrangement.

Self employed salary calculator estimates of the required appropriate PAYG instalment amounts can guide the sole trader as to an approximate amount that they will need to pay for an installment, but steady bookkeeping throughout the year to record payments and to calculate how much tax to set aside will provide more certainty as to whether income taxes are being properly prepared.

GST

Once self employment income reaches a threshold of $75,000 per annum, or could be projected to reach that threshold based on current revenue, sole traders are required to register for GST. GST must be accounted for on any invoices issued to Australian customers, clients and businesses from that point forward, by adding a 10% GST charge item.

For the self employed who also work another job, only income produced through self employment counts towards this threshold. Registration needs to occur before the threshold is reached, or within 21 days, to avoid fines and interest penalties on GST that should have been paid.

If any part of self employment involves ride-share (ride-sourcing) services, whereby the sole trader provides taxi or limousine travel for passengers, GST registration becomes compulsory, regardless of income earned.

The advantage of registering for GST is that any GST paid on goods and services purchased for the business (equipment such as cameras or business-related expenses such as web hosting, for example) can be claimed back. Rigorous bookkeeping processes will need to be put in place to track these GST collections and payments throughout the year.

A sole trader can register for GST voluntarily, before reaching the $75,000 business turnover threshold, in order to set up invoicing that accounts for GST early. This avoids the necessity to increase prices or reduce charges later when the business grows. It may also work to the sole trader’s advantage to be able to claim GST credits (on goods and services purchased for the business) or to present themselves as a more established and professional business.

An ABN is required to register for GST. Registration for GST can be completed through the “registrations” section of the ATO’s Business Register Portal.

Once registered, the ATO will typically send quarterly notices to lodge a Business Activity Statement (BAS). These statements detail GST amounts collected as part of the sole trader’s business activities and let the sole trader claim GST credits, for GST paid on items purchased for business use.

Step 3: establish bookkeeping for tax minimisation through deductions

With a business structure set to account for income tax and GST, tax deductions come into play.

A tax deduction refers to the subtraction of a business cost from the sole trader’s income. The net income left over is what the income tax rate is applied to.

Deductions can minimise tax burden, but claiming them requires thoroughly documented evidence of expenditures and activities, requiring attention to bookkeeping year-round, not just when submitting tax returns.

A tax minimisation strategy identifies possible deductions in advance of the upcoming taxation period so that documentation collection and bookkeeping requirements can be anticipated.

Here are some common deductions that sole traders can claim using documented invoices and records:

– Advertising and marketing costs

– Business website costs

– Travel and accommodation expenses, related to business and explicitly not associated with leisure

– Vehicle expenses, when a vehicle is purposed for travel to meet clients or suppliers

– Home office expenses, which may include a calculated portion of rent or mortgage, and a portion of property-related expenses such as council rates, land taxes and home and contents insurance

– A portion of utilities, home repairs and maintenance costs

– Professional development costs, such as classes and seminars related to the business activity or professional field, and memberships to professional organisations relevant to business activities

– Tax preparation costs, including bookkeeping and expenses incurred in using a tax agent to prepare and lodge activity statements and tax returns.

Deductions can require specific activity logging and paperwork collection throughout the year. Pherrus Financial Services’ tax advice and tailored tax consulting services are available to go through the details.

Step 4: develop a tax minimisation strategy that anticipates eligibility for tax breaks and benefits

As a sole trader, you may be eligible for instant write-offs on certain equipment purchases, qualify for deductions on pre-paid expenses, be able to claim deductions incurred during the set up of your business before you began receiving income, or qualify for certain capital gains tax concessions.

Are you self employed? Pherrus Financial Services can help

This article provides a general overview of taxation and tax management strategies for the self employed.

Without professional guidance, legally compliant reporting of income to the Australian Tax Office (ATO), careful administration of Goods and Services Tax (GST), and the ongoing management of timely and relevant bookkeeping entries for income tax minimisation can be stressful and onerous tasks that distract you from your business.

For professional tax planning advice and bookkeeping solutions for your specific business needs, help is available. Contact Pherrus Financial Services today for tax advice and tailored tax consulting services to maximise the financial benefits of your self employment.